BYD ATTO 3

INDIA'S PREMIUM ELECTRIC SUV

A perfect blend of performance, technology, sustainability and style.

TATA NEXON EV

THE GAME CHANGER

India's most loved electric SUV with enhanced range and features.

MG CYBERSTER

THE FUTURE, UNLEASHED.

An all-electric roadster combining thrilling performance with futuristic design.

MAHINDRA BE 6

BORN ELECTRIC.

Futuristic electric SUV delivering bold design, smart technology, and thrilling performance.

Tata Harrier EV

POWER. PRESENCE. ELECTRIFIED.

Bold SUV capability meets next-generation electric performance and intelligent technology.

Latest EV

View All EV

EV

Citroen eC3 X Price Guide 2026: Specs, Real Range &…

Citroen eC3 X Quick Overview The Citroen eC3 X represents an accessible and highly…

EV

EV

Tesla S vs X vs Y: 2026 Buyers Comparison

Tesla S vs X vs Y Quick Overview The choice between the Tesla Model…

EV

EV

Tesla Semi Price Guide 2026: Range, Specs, Battery & Fleet…

Tesla Semi Quick Overview The 2026 Tesla Semi marks the entry of high-volume mass…

Latest Cars

View All Cars

Cars

Suzuki Wagon R Custom Z HYBRID ZX 2026: Specs, Real…

Suzuki Wagon R Custom Z HYBRID ZX Quick Overview The Suzuki Wagon R Custom…

Cars

Cars

Mercedes-Benz S-Class Price Guide 2026: Specs, Plug-In Hybrid & Review

Mercedes-Benz S-Class Quick Overview The newly launched Mercedes-Benz S-Class Facelift reclaims its throne as…

Cars

Cars

Mini Countryman C Price Guide 2026: Specs, Real Mileage &…

Mini Countryman C Quick Overview The Mini Countryman C represents the largest, most family-oriented…

Latest Bikes

View All Bikes

Bikes

Bajaj Avenger 400: Expected Price, Launch Date, Specs & Cruiser…

What You Need to Know About the Bajaj Avenger 400 The Bajaj Avenger 400…

Bikes

Bikes

Yamaha R15 Review: Performance, Mileage, Features & Real-World Riding Experience

What You Need to Know (At a Glance) The Yamaha R15 is a premium…

Bikes

Bikes

Bajaj Pulsar NS200 Review: Performance, Mileage, Features & Riding Experience

What Makes the Bajaj Pulsar NS200 Stand Out? The Bajaj Pulsar NS200 is a…

Cars Under 10 Lakh

View All EV

EV

MG Comet EV Price Guide 2026: Real-World Range, Interior &…

MG Comet EV Quick Overview The MG Comet EV is an ultra-compact, two-door urban…

EV

EV

Tata EV Price Guide 2026: Tata Punch EV Price &…

Quick Summary for Busy Readers The 2026 Tata Punch EV is positioned as a…

Cars

Cars

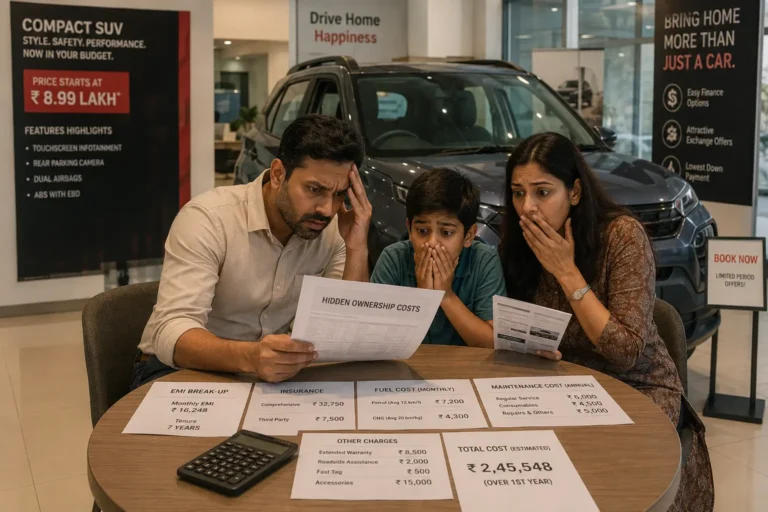

Hidden Costs of Buying Cars Under ₹10 Lakh: Real Ownership…

Quick Reality Check (The 2026 Truth) The showroom price of a car is just…

Cars Under 5 Lakh

View All Comparisons

Comparisons

Petrol vs CNG Cars Under ₹5 Lakh: 2026 Running Cost…

The Petrol vs CNG Cars Real Difference in Short In 2026, CNG cars are…

Comparisons

Comparisons

Hatchback vs Sedan Under ₹5 Lakh: Real Comparison 2026

In 2026, the choice between a hatchback and an entry sedan under ₹5 lakh…

Comparisons

Comparisons

Maruti Alto K10 vs Renault Kwid: Best Car Under ₹5…

In 2026, the choice between the Maruti Alto K10 vs Renault Kwid comes down…

Trending Now

View All

Cars

Suzuki Wagon R Custom Z HYBRID ZX 2026: Specs, Real…

Suzuki Wagon R Custom Z HYBRID ZX Quick Overview The Suzuki Wagon R Custom…

India Car News

India Car News

E20, E30 & E85 Flex-Fuel Cars in India 2026: Models,…

E20, E30 & E85 Flex-Fuel Cars in India Quick Overview India’s automotive landscape has…

India Car News

India Car News

Tata Sierra EV Teased Again Ahead of Launch: 7 Things…

Tata Motors has once again teased the much-awaited Tata Sierra EV, giving enthusiasts another…

Editor's Pick

View All EV

EV

Mahindra XEV 9e Price Guide 2026: Range, Running Cost, interior…

Mahindra XEV 9e Overview The 2026 Mahindra XEV 9e is a premium, born-electric luxury…

Cars

Hidden Costs of Buying Cars Under ₹10 Lakh: Real Ownership…

Quick Reality Check (The 2026 Truth) The showroom price of a car is just…

Cars

Cars

🚗Best Cars Under ₹10 Lakh in India (2026 Edition): Mileage,…

Best Cars Under ₹10 Lakh in India (2026) – Quick Overview Cars under ₹10…

Comparions

View All Comparisons

Comparisons

BMW Z4 vs MG Cyberster 2026: The Ultimate Luxury Roadster…

BMW Z4 vs MG Cyberster Quick Overview In 2026, the BMW Z4 M40i (priced…

Comparisons

Comparisons

MG Windsor EV vs Tata Nexon EV 2026: Battle of…

MG Windsor EV vs Tata Nexon EV Quick Overview In 2026, the Tata Nexon…

Comparisons

Comparisons

Mahindra BE 6 vs Mahindra XEV 9e 2026: Battle of…

Mahindra BE 6 vs Mahindra XEV 9e Quick Overview In 2026, the Mahindra BE…